by Elsa Soto | Dec 19, 2020 | Blog, Buyers, Homeowners, Homes, Villas and Condos, Investment Property in Florida, News, Real Estate News, Renters, Sellers

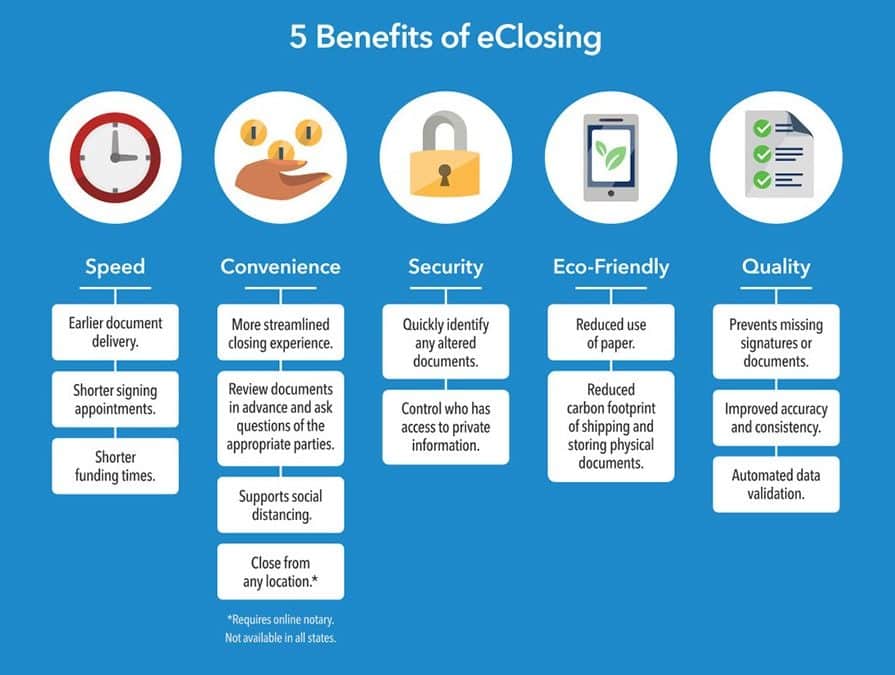

Online Closings are here! Learn about digital closings and how to get your practice ready. Real estate closings will change over the next 2-3 years and move in the direction of less paper and more technology. Lenders are recognizing the efficiency and cost savings...

by Elsa Soto | Nov 29, 2020 | Blog, Homeowners, Mortgages, Real Estate Components, Real Estate News

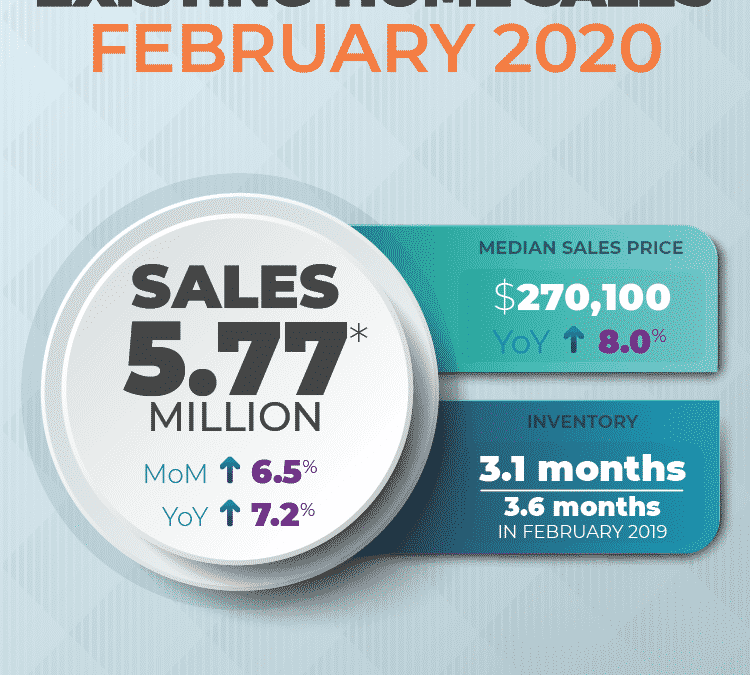

WASHINGTON (November 19, 2020) – October Home Sales Report shows and upward trend marking five consecutive months of month-over-month gains, according to the National Association of Realtors®. All four major regions reported both month-over-month and year-over-year...

by Elsa Soto | Nov 13, 2020 | Blog, Buyers, Homeowners, Homes, Villas and Condos, Investment Property in Florida, Mortgages, News, Real Estate News, Renters, Sellers

For veterans and active military, VA loans are a great way to achieve the dream of homeownership. More than 22 million service members have used these flexible, no down payment loans since 1944.But when people hear “no down payment,” they often don’t realize...

by Elsa Soto | Nov 13, 2020 | Blog, Buyers, Homeowners, Real Estate News, Renters, Sellers

Lenders establish a required “loan to value” or “LTV” for each loan program, even loans that do not require a down payment. The property is the lender’s collateral in the transaction and an independent appraisal will help support the value of the subject property....

by Elsa Soto | Mar 30, 2020 | Blog, Homeowners, Homes, Villas and Condos, Investment Property in Florida, Real Estate News

Existing-home sales climbed substantially in February after a slight decline in January, according to the National Association of Realtors®. Of the four major regions, only the Northeast reported a drop in sales, while other areas saw increases, including sizable...