by Elsa Soto | Dec 16, 2019 | Blog, Mortgages, Real Estate News

Financing a home is one of the most critical factors for buyers looking to purchase real estate. Here are some suggestions on How to Finance a Home Creatively that you may not have been aware of. Investigate local, state, and national down payment assistance...

by Elsa Soto | Dec 9, 2019 | Blog, Buyers, Mortgages, News, Real Estate Components, Real Estate News

Term.Mortgages are generally available at 15-, 20-, or 30-year terms. In general, the longer the term, the lower the monthly payment. However, shorter terms mean you pay less interest over the life of the loan.Fixed vs. adjustable interest rates.A fixed rate allows...

by Elsa Soto | Nov 18, 2019 | Blog, Buyers, Mortgages, News, Real Estate News

Loan terms, rates, and products can vary significantly from one company to the next. When shopping around, these are a few things you should ask about.General questions:What are the most popular mortgages you offer? Why are they so popular?Are your rates, terms, fees,...

by Elsa Soto | Oct 21, 2019 | Blog, Mortgages, Real Estate News

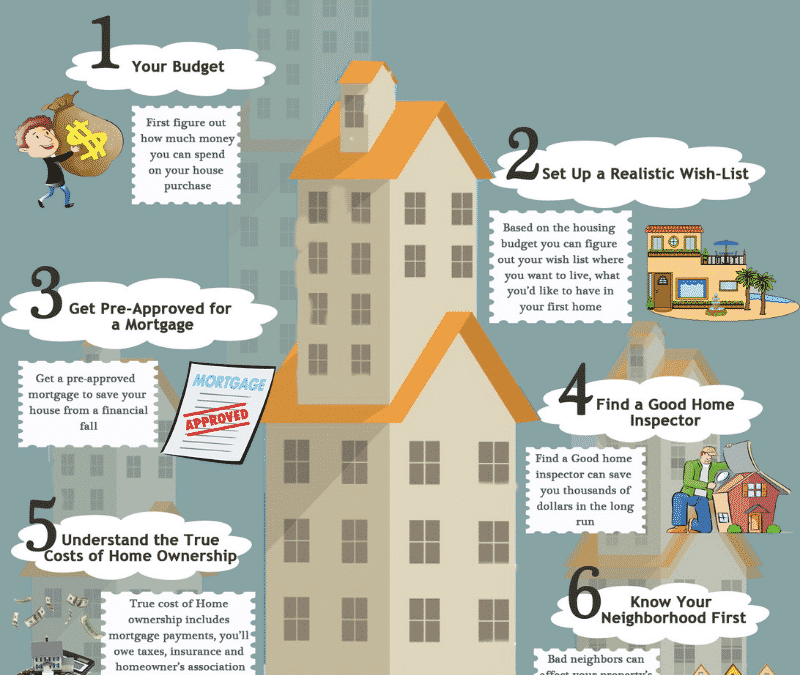

Develop a budget.Instead of telling yourself what you’d like to spend, use receipts to create a budget that reflects your actual habits over the lastseveral months. This approach will better factor in unexpected expenses alongside more predictable costs such as...

by Elsa Soto | Mar 18, 2019 | Blog, Buyers, Mortgages, News, Property for Sale in Orlando, Real Estate Components, Real Estate News

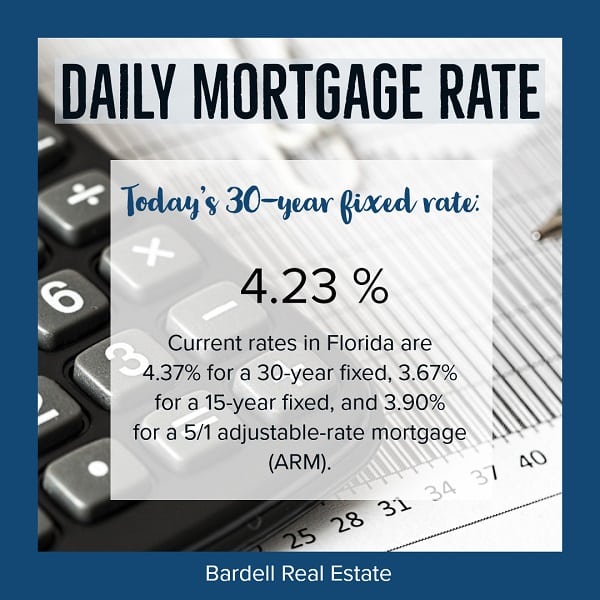

Central Florida’s Daily Mortgage RatesWelcome to this weeks snapshot of Central Florida Daily Mortgage Rates! Does your New Year’s Resolution include spending time to invest your hard earned money into something that will continue to reward you, especially...