by Elsa Soto | Jun 1, 2020 | Blog, Buyers, News, Real Estate Components, Real Estate News, Renters, Sellers

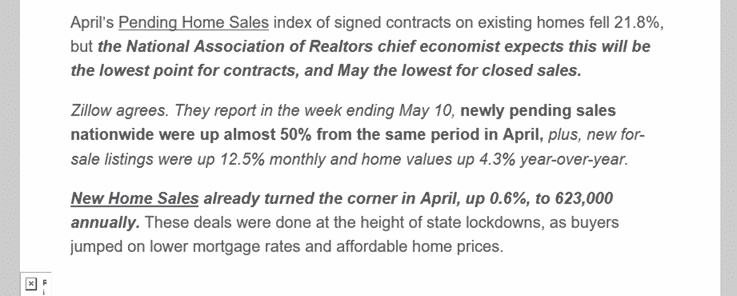

Stay-at-home orders to prevent the spread of coronavirus put a major dent in the number of contracts that were signed in April, The index of pending home sales dropped 21.8% in April compared to March as the coronavirus pandemic kept prospective home-buyers out of the...

by Elsa Soto | May 21, 2020 | Blog, Local Events, News, Press Releases, Real Estate News, Things to Do in Orlando

Home buyer IncentivesBe sure you’re sending the right message to buyers when you throw in a homebuyer incentive to encourage them to purchase your home.When you’re selling your home, the idea of adding a sweetener to the transaction — whether it’s a decorating...

by Elsa Soto | May 14, 2020 | Blog, Press Releases, Real Estate News

ORLANDO, Fla. – In the first quarter of 2020, Florida’s housing market reported higher median prices and more closed sales compared to a year ago, though the coronavirus pandemic’s impact on the state’s economy and real estate markets began to emerge in mid-March,...

by Elsa Soto | May 11, 2020 | Blog, Buyers, Real Estate News

How long does it take to improve your credit score? Having good credit helps you prove your creditworthiness to potential lenders. If you’re hoping to buy a home, having a good credit score is key, since it helps you qualify for a mortgage. So if your credit...

by Elsa Soto | May 6, 2020 | Blog, Real Estate Components, Sellers

When buying a house is high on your priority list and you spot The One—the property that has everything you’ve ever dreamed of and more—it can be tempting to put pedal to the metal and close the deal as quickly as possible. But slow down! You need to ask lots of...