by Elsa Soto | Aug 9, 2022 | Blog, Homeowners, Homes, Villas and Condos, News, Real Estate News, Sellers

The 7 Deadly Sins of Home Selling Today In recent years, home sellers have enjoyed bidding wars that have driven property prices sky-high. However, things are finally turning around. In short, rising interest rates, rampant inflation, and the threat of recession are...

by Elsa Soto | Aug 5, 2022 | Blog, Homeowners, News, Property Management, Real Estate News, Renters

Pros of Hiring Property Management Pros of Hiring Property Management At some stage in their rental management journey, most landlords inevitably confront a crucial choice: should they engage a property manager or not? This question may arise when a landlord...

by Elsa Soto | Aug 3, 2022 | Blog, Buyers, Homeowners, News, Real Estate News

HOA Due Diligence Guide Before Buying HOA Due Diligence Guide Before Buying If you’re thinking about buying a home in a homeowners association, don’t worry, you’re not alone. According to iProperty Management & Investments, more than half (53%)...

by Elsa Soto | Aug 2, 2022 | Blog, Homeowners, Homes, Villas and Condos, News, Real Estate News

Is Lakeland’s Real Estate Market Overtaking Most Florida Metro Areas? Is Lakeland’s Real Estate Market Overtaking Most Florida Metro Areas? The Lakeland FL Real Estate Market recorded the 3rd highest YOY increase in median home price out of all US Metro areas in...

by Elsa Soto | Jul 29, 2022 | Blog, Homeowners, Homes, Villas and Condos, News, Property Management, Real Estate News, Renters

Here’s Where Florida’s Rental Markets Rank Here’s Where Florida’s Rental Markets Rank By Dave Berman Miami charges the seventh-highest average rent in the nation and is No. 1 in Fla. at $2,846. Jacksonville is Fla.’s least expensive with rent averaging $1,748....

by Elsa Soto | Jul 27, 2022 | Blog, Homeowners, Homes, Villas and Condos, News, Real Estate News, Sellers

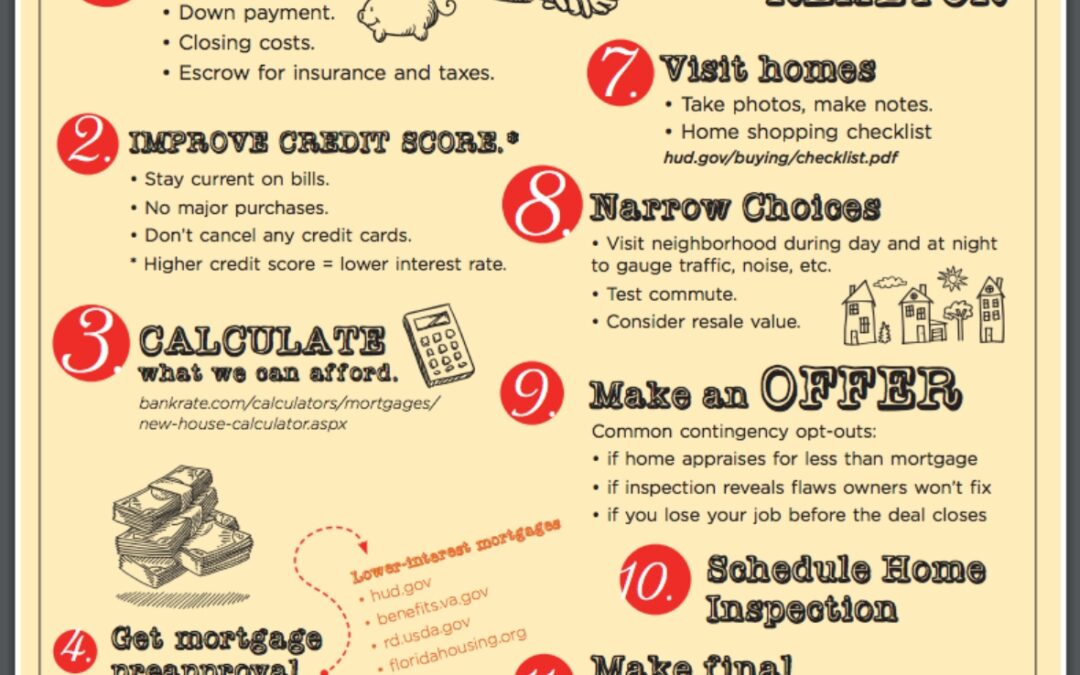

List for First-time Buyers To – Do List for First-Time Buyers 1. Save Down payment Closing Costs Escrow for insurance and taxes 2. Improve Credit Score Stay current on bills No major purchases Don’t cancel any credit cards Higher credit score = lower...