by Elsa Soto | Dec 31, 2018 | Blog, Buyers, Homeowners, Mortgages, News, Real Estate Components

Central Florida’s Daily Mortgage Rates Welcome to this weeks snapshot of Central Florida Daily Mortgage Rates! Does your New Year’s Resolution include spending time to invest your hard earned money into something that will continue to reward you,...

by Elsa Soto | Nov 26, 2018 | Blog, Buyers, Homeowners, Mortgages, News, Property for Sale in Orlando, Real Estate News

Central Florida’s Daily Mortgage Rates Welcome to this weeks snapshot of Central Florida Daily Mortgage Rates! Now has never been a better time to invest your hard earned money into something that will continue to reward you, especially with ownership!...

by Elsa Soto | Nov 21, 2018 | Blog, Buyers, Homes, Villas and Condos, Mortgages, New Construction, News, Property for Sale, Property for Sale in Orlando

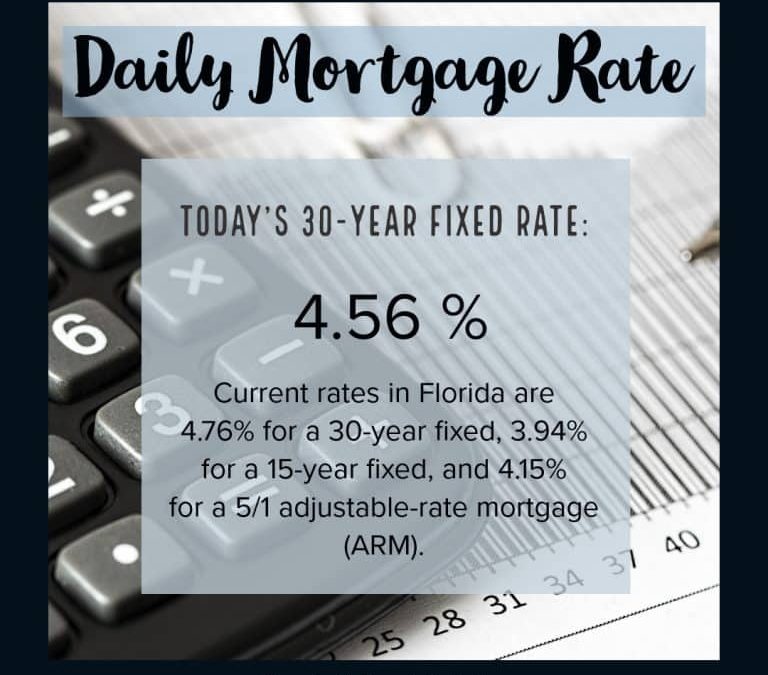

Central Florida’s Daily Mortgage Rates Welcome to this weeks snapshot of Central Florida Daily Mortgage Rates! Now has never been a better time to invest your hard earned money into something that will continue to reward you, especially with ownership! Source:...

by Elsa Soto | Nov 12, 2018 | Blog, Homes, Villas and Condos, Mortgages, News, Property for Sale in Orlando, Real Estate Components, Real Estate News

Central Florida’s Daily Mortgage Rates Welcome to this weeks snapshot of Central Florida Daily Mortgage Rates! Now has never been a better time to invest your hard earned money into something that will continue to reward you, especially with ownership!...

by Elsa Soto | Oct 31, 2018 | Blog, Buyers, Homeowners, Investment Property in Florida, Mortgages, News, Property for Sale, Real Estate Components

Taking FEAR Out of the Mortgage Process A considerable number of potential buyers shy away from jumping into the real estate market due to their uncertainties about the buying process. A specific cause for concern tends to be mortgage qualification. For many, the...