by Elsa Soto | Dec 31, 2024 | Blog, Homeowners, Sellers

As the holiday season winds down and the Christmas decorations are packed away, the start of the new year presents the perfect opportunity to refresh your home and set it up for a successful sale in the coming months. With the holidays behind us, now is the time to...

by Elsa Soto | Dec 31, 2024 | Blog, Buyers, Homeowners, Homes, Villas and Condos, Investment Property in Florida, Sellers

Owning a vacation home can be a dream, but it requires proper maintenance and care to avoid costly issues. Unlike primary residences, vacation homes often remain vacant for extended periods, which can lead to problems if not properly managed. Plumbing failures, storm...

by Marketing | Dec 4, 2024 | Buyers, Homeowners, Mortgages, New Construction, News, Property for Sale, Property for Sale in Orlando, Real Estate News, Renters, Sellers

Real Estate Outlook for 2025: Key Trends and Predictions The housing market has faced challenges in recent years, but brighter days may be ahead. Lawrence Yun, Chief Economist at the National Association of REALTORS® (NAR), shared an optimistic forecast for 2025 and...

by Marketing | Dec 2, 2024 | Blog, Buyers, Homeowners, Homes, Villas and Condos, Long Term Rental, Property Management, Sellers, Uncategorized

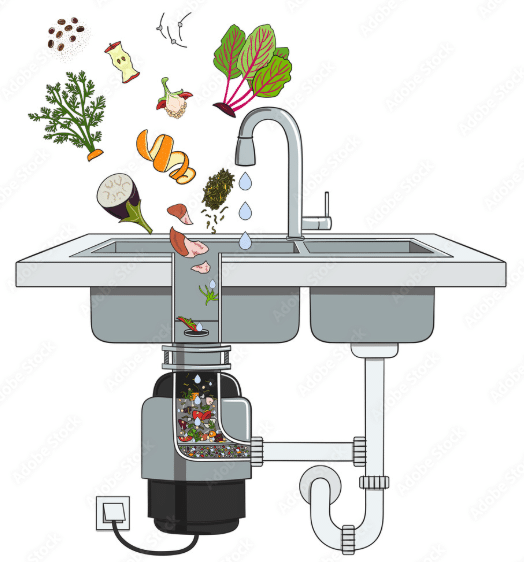

Property Management Spotlight: Tips for Extending the Lifespan of your garbage disposal Keeping up with your home’s garbage disposal might seem like a small task, but it has huge benefits. As our property expert Lucy Hinson explains, regular upkeep of this important...

by Marketing | Oct 2, 2024 | Blog, Buyers, Homeowners, Real Estate News, Renters, Sellers

Understanding Buyer Broker Agreements: What You Need to Know Understanding Buyer Broker Agreements: What You Need To Know Buying a home is a major life decision, and at RE/MAX Heritage, we believe that you should feel supported throughout the process. One of the ways...

by Elsa Soto | Jul 10, 2024 | Blog, Buyers, Homeowners, News, Real Estate News, Renters, Sellers

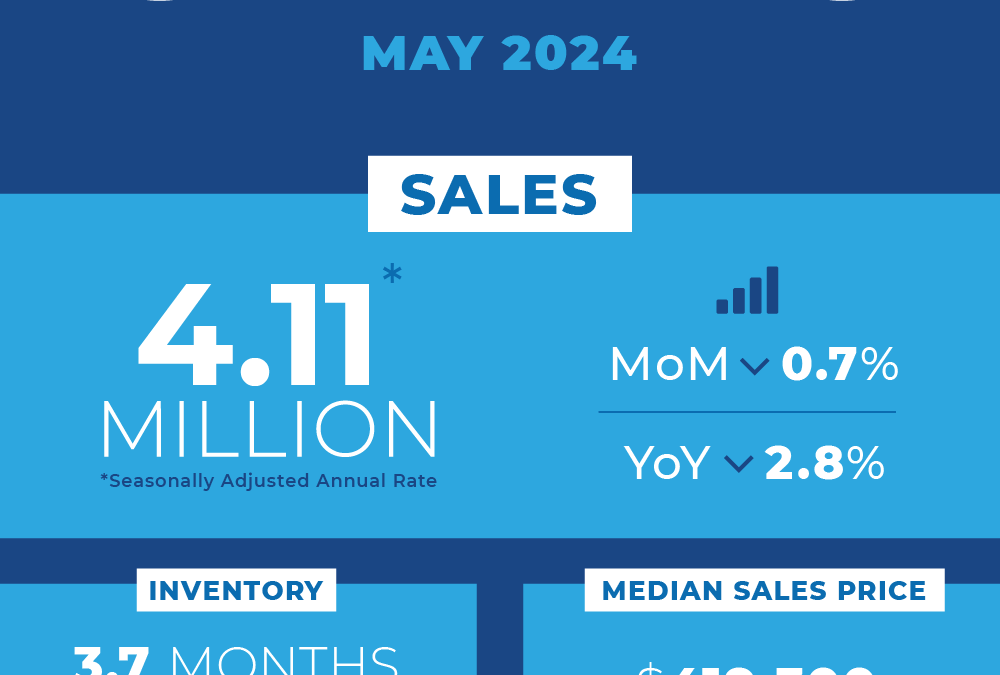

Real Estate Sales Report May 2024 Real Estate Sales Report May 2024 Existing-home sales slightly declined in May while the median sales price reached a record high, as reported by the National Association of REALTORS® (NAR). Sales fell month-over-month in the South...