by Elsa Soto | Dec 3, 2019 | Blog, Buyers, News, Real Estate Components, Real Estate News, Sellers

The term “agency” is used in real estate to help determine what legal responsibilities your real estate professional owes to you and other parties in the transaction.The buyer’s representative (also known as a buyer’s agent) is hired by prospective buyers and...

by Elsa Soto | Nov 22, 2019 | Blog, Buyers, Homeowners, Homes, Villas and Condos, Investment Property in Florida, Property for Sale in Orlando, Real Estate Components, Real Estate News, Renters, Sellers

Existing-home sales rose in October, a slight recovery from the declines seen in September, according to the National Association of Realtors®. The four major U.S. regions were split last month, with the Midwest and the South seeing growth, and the Northeast and the...

by Elsa Soto | Sep 19, 2019 | Blog, Homeowners, Homes, Villas and Condos, Press Releases, Real Estate Components, Real Estate News

The Existing-home sales inched up in August, marking two consecutive months of growth, according to the National Association of Realtors®.Total existing-home sales completed transactions that include single-family homes, town homes, condominiums and co-ops, rose 1.3%...

by Elsa Soto | Mar 25, 2019 | Blog, Buyers, Homeowners, Mortgages, News, Real Estate Components, Real Estate News

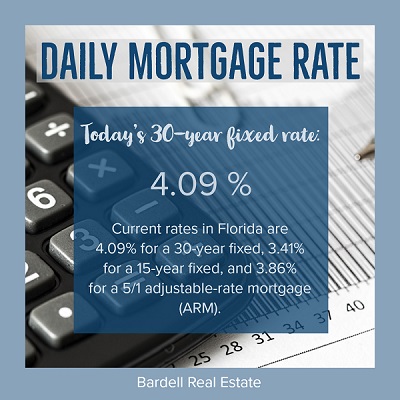

Central Florida’s Daily Mortgage RatesWelcome to this weeks snapshot of Central Florida Daily Mortgage Rates! Does your goal list include spending time to invest your hard earned money into something that will continue to reward you, especially with ownership?...

by Elsa Soto | Mar 18, 2019 | Blog, Buyers, Mortgages, News, Property for Sale in Orlando, Real Estate Components, Real Estate News

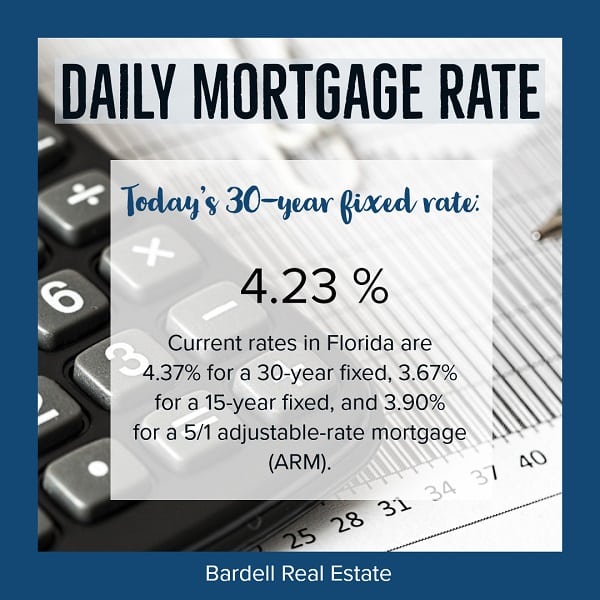

Central Florida’s Daily Mortgage RatesWelcome to this weeks snapshot of Central Florida Daily Mortgage Rates! Does your New Year’s Resolution include spending time to invest your hard earned money into something that will continue to reward you, especially...

by Elsa Soto | Jan 29, 2019 | Blog, Homes, Villas and Condos, Local Events, Mortgages, Real Estate Components, Real Estate News

Central Florida’s Daily Mortgage Rates Welcome to this weeks snapshot of Central Florida Daily Mortgage Rates! Does your New Year’s Resolution include spending time to invest your hard earned money into something that will continue to reward you,...