Fla.’s Oct. Housing Market: Median Prices, Inventory Rise

Fla.’s Oct. Housing Market: Median Prices, Inventory Rise

Fla.’s Oct. Housing Market: Median Prices, Inventory Rise

ORLANDO, Fla., Nov. 18, 2022 /PRNewswire/ — Florida’s housing market reported higher median prices and more inventory (active listings) in October compared to a year ago, though inflation and rising interest rates remained a factor for buyers, according to Florida Realtors®’ latest housing data.

Closed sales of single-family homes statewide last month totaled 20,837, down 24.6% year-over-year, while existing condo-townhouse sales totaled 8,356, down 26.9% from October 2021, according to data from Florida Realtors Research Department in partnership with local Realtor boards/associations. Closed sales may occur from 30- to 90-plus days after sales contracts are written.

According to Florida Realtors Chief Economist Dr. Brad O’Connor, a look at market conditions from 2021 to the latter half of 2022 offers insight into how sales have been affected. He explained, “The beginning of 2022 marked the end of a nearly two-year period of record-low mortgage rates, as the Fed began to reverse its course in order to fight pervasive inflation in the economy. The rapid pace of the resulting increases in interest rates has dramatically increased the monthly payments required for new mortgages, and home price growth has only recently started to show signs of responding.

“In terms of closed sales in Florida, 2022 started out a lot like 2021, but soon, the shock of the rapid rise in mortgage rates caused many buyers to suspend their home searches and sit on the fence; some even had to drop out when their planned budget for a home couldn’t keep pace. As a result, the second half of 2022 has seen the level of existing home sales in Florida more-or-less fall in line with the typical pre-pandemic seasonal trends.”

O’Connor added, “The fact that monthly sales still remain in the neighborhood of pre-pandemic levels despite today’s significantly higher home prices and mortgage rates only illustrates that despite these headwinds, housing demand in Florida continues to receive support from its recent surge in post-pandemic in-migration, vacation home purchases, and the ever-increasing number of millennials looking to find a home for their growing families.”

In October, the statewide median sales price for single-family existing homes was $401,990, up 12% from the previous year; for condo-townhouse units, it was $310,000, up 19.2% over the year-ago figure. The median is the midpoint; half the homes sold for more, half for less.

“The supply of for-sale homes continues to slowly build, easing inventory constraints in many markets across the state,” said 2022 Florida Realtors® President Christina Pappas, vice president of the Keyes Family of Companies in Miami. “Having more supply available will begin to ease some of the pressure on home prices, which in turn will help buyers dealing with higher interest rates. Homes in Florida continue to go under contract quickly, though the time to contract is slightly increasing: The median time to contract for single-family existing homes last month was 25 days compared to 12 days during the same month a year ago. The median time to contract for existing condo-townhouse units was 25 days compared to 15 days in October 2021.

“Buying or selling a home is a complex and emotional process but working with a local Realtor can help you understand changing market conditions and give you peace of mind.”

Statewide inventory was higher last month than a year ago for both existing single-family homes, up 88.4%, and for condo-townhouse units, up 31%. The supply of single-family existing homes increased to a 2.7-months’ supply while existing condo-townhouse properties were at a 2.5-months’ supply in October.

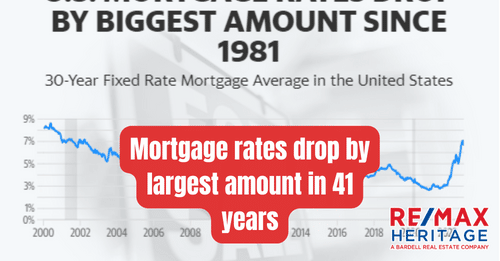

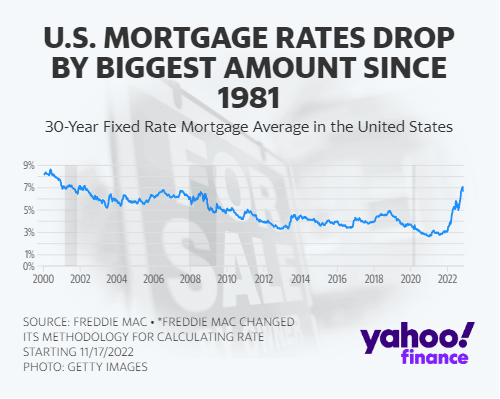

According to Freddie Mac, the interest rate for a 30-year fixed-rate mortgage averaged 6.90% in October 2022, significantly up from the 3.07% average during the same month a year earlier.

To see the full statewide housing activity reports, go to the Florida Realtors Newsroom at http://floridarealtors.org/newsroom and look under Latest Releases or download the October 2022 data report PDFs under Market Data at: http://floridarealtors.org/newsroom/market-data.

Florida Realtors® serves as the voice for real estate in Florida. It provides programs, services, continuing education, research and legislative representation to its more than 225,000 members in 51 boards/associations. Florida Realtors® Newsroom website is available at http://floridarealtors.org/newsroom.

SOURCE Florida Realtors

Experts in Residential Real Estate in Orlando

If you are buying or selling real estate it’s quiet often the single most important financial decision you make. For the last 30 years we have helped clients buying and selling property in Orlando and the surrounding areas. Put simply, this means the knowledge and expertise accumulated over this time ensures our clients get the best representation possible.

Our experienced agents will help and guide you through the entire process providing valuable support every step of the way.

Ready to make a Move?

Bardell Real Estate are the experts in helping you with your selling, buying or renting needs near Orlando, Florida. Make your Disney area experience a forever memorable one. Call us now to speak to a real estate agent.